Non-Trivial Economic Mistakes - Part I

How to be a better macroeconomist than Noahpinion

Most of my readers will be familiar with some economic fallacies. You probably know better than to fall for sunk costs and understand that you have to adjust prices and/or salaries for inflation. But there’s a range of economic fallacies that Econ 101 does not bang into your head directly. These are very common in life and sometimes lead to terrible mistakes. Thankfully, I’m here to write a Substack post about it.

Only Comparing Benefits or Costs

One common statement I heard during the pandemic went something like this: “we’ve shut down schools, but we have not shut down public transportation, how is this consistent?”. The person asking the question clearly implied that the risks of infection were just as great from public transportation, therefore, a policy regulating one should also regulate the other.

This reasoning falls flat as it only views one side of the costs vs benefits equation. Indeed, public transportation may have been a larger Covid-19 risk than schools, but schools can at least partially be replaced with online education tools such as Zoom. No such option is available to replace buses and subways. In other words, the person asking the question only compared the benefits of regulating schools and transportation, but not the costs.

After hearing about this once, you’ll notice it everywhere. Another clear example here is the often-mistaken belief that if the United States or some other country did not do something, they were not capable of doing it. In reality, it could simply have been that it was not worth the costs. In fact, I assure you, that if the US thought “winning” in Afghanistan was dreadfully important, they would have sent in two hundred thousand soldiers and stayed for another 20 years.

Ex Ante vs Ex Post

Suppose you observe someone execute a risky political maneuver. Say, an US President incited a mob to overthrow the results of an election. Say that people said this was a huge mistake and would end his political career. Say that he then went on to win the next presidential election regardless. Purely hypothetical of course. Many would rush to crown this hypothetical President as a political genius. He takes bold risks and they pay off.

But this betrays a fundamental confusion between ex ante payoffs and ex post payoffs. Your action may have turned out fine, but that does not mean it was the right choice. The right way to think about this is as a terrible lottery that you just happen to win. You’re about to roll a pair of dice. If you get two sixes, you win five million dollars. If you don’t roll two sixes, you lose five million. You roll two sixes and live happily ever after. Was this the right decision? No, you’re just an utter idiot who got lucky.

This fallacy also appears everywhere if you look for it. If the Invasion of Ukraine ends on Putin’s terms, people will laud him as a strategic genius, even as the decision to begin the war was a completely stupid risk with extremely negative payoffs.

So do not judge leaders by their intentions and do not judge them by their results. Judge them by the expected results of their actions.

Constant vs Current PPP

This will be a very simple one.

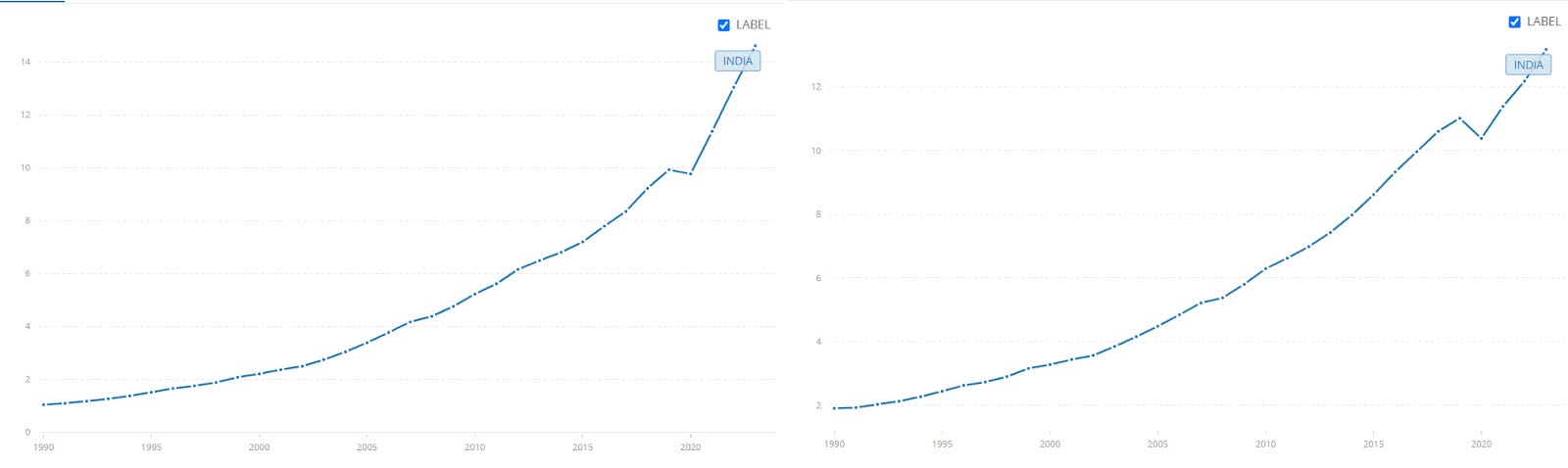

Above you see two graphs of India’s GDP adjusted for purchasing power. Do you see a difference? The numbers seem to be somewhat off and the graph on the left appears to have a steeper slope.

This is because there are two ways to adjust for PPP. The graph on the left is called “current international $” while the one on the right is “constant 2021 international $”. The one on the left adjusts for differences in purchasing power between countries and is very apt for comparing the GDP of different countries at the same point in time but it does not adjust for the inflation of the dollar. The graph on the right on the other hand makes both of these adjustments and is the correct metric to use if you plan on tracking a country’s economic performance over time.

Sidenote: this is a mistake I’ve seen some extremely seasoned economic commentators make. So beware that it will be quite common in the wild!

Fisher Equation

The Fisher equation is one of the most important equations of macroeconomics. It states that the real interest rate is the nominal rate net of inflation.

Unfortunately, it has been greatly misinterpreted. One common mistake regarding the Fisher equation is to think of the real interest rate as fixed and as something that central banks cannot affect. When one reasons like this, they conclude that inflation can be lowered if nominal interest rates are lowered. This has led to the disaster that is the Turkish economy.

The reality is much stranger. Central banks raise interest rates and thereby lower inflation. But if they want a higher long-run nominal rate, they’ll have to raise inflation to make that happen. Does that make no sense to you? Good, then you can read my piece on monetary policy.

Make sure you catch part two which will include: (1) the importance of expectations (2) that even causation does not imply correlation (3) the importance of income and substitution effects (4) whether savings are good or bad for the economy.

Great post!

Another way to frame the Ex Ante vs Ex Post distinction is from decision making theory, where you should judge decisions not (only) by the outcome but by the process and assumptions with which the decision was made.

As for the fisher equation, neofisher interpretations do not rely on a fixed real rate. That is a common misconception.

In fact, conventional monetary policy requires "amplified transmission", that is, nominal rate changes must induce an even greater change to the real rate, to acheive deflation.

For example, if you raise nominal rates by 2%, and real rates increase 2%(perhaps from -1% to +1%), then no change to inflation happens. You in fact need a real rate change of 3%, in order to induce 1% deflation, when you increase nominal rates by 2%.

The long run nominal rate setting is in essence a "benchmark" for the real rate. the real rate must meet or exceed the nominal rate to have 0% inflation. If you are okay with 2% inflation, then the real rate must be within 2% of the nominal rate, to hit that target.

Thus the higher the nominal rate, the higher the real rate you need to hit your target.

The conventional view is justified on the premise that the real rate is accelerating, thus you need to correct the real rate before you can stabilize inflation. But if you raise rates too quickly, arguably you prevent inflation from correcting the price of an overvalued currency, ie the national debt is too big. Whereas if you wait sometime, the value of the national debt can correct downward, before you attempt to stabilize the real rate.

Conventional monetary theory is 100% based on the premise you need to correct real rates first, and immediately, but arguably there is a better way which involves waiting for inflation to mostly run its course before hiking rates, and that waiting is better because it doesn't lead to an explosion of interest on the national debt, until growth is poised to recover.